INVESTORS SHOULD HEAD FOR THE HILLS

Nobody knows, what the markets are up to. The markets can do anything, because market participants act on emotion and on the basis of expectations, which are often irrational. Unfortunately, irrational actions are only confirmed in hindsight, because they seemed perfectly rational at the time. Therefore, prudent investors are nearly always pulling the plug too early and look pretty foolish for awhile, when doing so. The crowd usually succumbs to herd-like behaviour and loses big time, later.

What if massive monetary easing (QE) fails? Or if it has titanic (!) unintended consequences? Mind you, with interest rates essentially at zero, or worse, at negative levels, the typical monetary policy of a Central Bank ceases to work. Extreme monetary stimulus distorts normal price discovery and traditional valuation parameters. But these false signals could actually be responsible for the Crash, that would inevitably follow. At some point, no investor would want to hold on to expensive assets. The expected future return on those assets would just be too low. Also, by now it has become increasingly clear, that the ‘real’ economy cannot benefit much as long as excessive debt levels are impeding debt servicing, even with low interest rates. The process of deleveraging to more sustainable levels, always takes its course, no matter how onorthodox monetary policies may have become.

The nightmare of the end of the extended rally in ‘risky assets’ is looming ever closer. Every boom is followed by a bust. Trouble is, that it may take decades to recover from the next bust. Participating in this boom would turn out to be very unwise indeed, because it would all have been for nothing. Moreover, the excessive (‘cheap’) leverage applied by market participants to their ‘trades’, virtually guarantees the total wipeout of many. It doesn’t matter, what the eventual trigger could be for the end of the party. It usually is a combination of factors, which will fan the flames. The herd, however, may focus on the wrong possible triggers, while ignoring the real ones.

Most of the massive global debt is pretty low quality. That’s why the colossal explosion in liquidity has led to a shortage of high-quality debt instruments. Therefore, there only seems to be a bubble in low-quality, not high-quality debt, because if the situation becomes uncontrollably chaotic, only the latter will be tradeable or ‘liquid’ at all. But ‘risky assets’ like stocks and other overpriced assets could decline 70% or more, as they usually do, after such cycles of euphoria. Low-quality debt could become wallpaper.

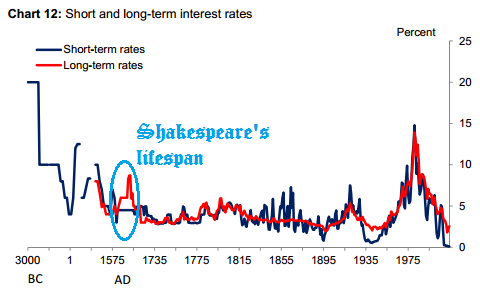

Make no mistake. The frantic flight into high-quality debt, even at negative yields, is only partially due to Quantitative Easing (QE), which hoovers up high-grade debt. Secular stagnation, deflationary pressures, portfolio rebalancing and demographics, all play their part as well. But most important of all, and probably missed by most experts, is the fact, that the current action of the high-quality bond market is the omen for the deepest economic depression in history, ever. Society would simply cease to function if negative interest rates are allowed to persist. This now appears to be a secular, irreversible, not temporary, phenomenon. It foreshadows the final unwinding of the Grand Super Cycle in CREDIT of the last 60 years. Are you ready?

RICK SCHMULL

March 18th, 2015

WESTCLIFF-On-SEA, Essex, U.K.

P.S. COMMENTS ARE DISABLED WITH IMMEDIATE EFFECT